I’ve joined Sutter Hill Ventures to find and build companies with our next generation of EIRs and CEOs.

Over the past several years of writing and working with founders I have been driven by the question of how our industry can best compound at creating companies that matter. What became clear is that the earliest stages of exploration are not only the least institutionally focused on. But also where it is most valuable. I was led to SHV early in the course of this exploration, and when the opportunity to join and help build its next chapter presented itself it was obvious I needed to accept it.

Few firms take the earliest stages of company formation seriously. The gravity of fund math pulls them away from the flux of building new things from the ground up. Much less doing it repeatedly. This raw experience with the formation stage and ability to generate outsized returns while focused on it, is what makes SHV special. There is a familiarity with the nebulosity that can only be developed from having repeatedly been through the founding journey from beginning to end.

SHV is instrumental when the clay is wet, in foundational companies that redefine their industries like Snowflake, Nvidia, and Pure Storage. It believes that the beginnings matter, even when they are at their most delicate and feel like they don’t. And in being a partner in the exploration of what is truly possible and worthwhile.

At its core, the team is focused on the art and science of creation. And what has impressed me most is their commitment to continuously redefine and refine themselves to serve founders through the nebulosity of the founding journey.

SHV understands that we cannot make starting companies easier. I don’t know that anyone can. But we can make that effort go further. And that can make all the difference.

In just the first few months here I am already grateful for the experiences of being at SHV and exploring with our EIRs. I’m excited to contribute to making SHV the best place for founders to create their life’s work.

If you have a vision for a future you want to pull forward, or you’re a deep technical expert, experienced executive, or repeat founder and would like to learn more, please reach out.

If the IPO process is like a debutante ball, the top investment banks are akin to a finishing school. They help gussy up companies, teach them proper manners like how to do GAAP accounting, and bring them around to call on prospective investors and eventually debut to society.

This is the role investment banks have played for decades, but in recent years this dynamic has begun to break down. Not in all sectors—in most sectors investment banks still occupy the same role—but in tech, the importance and role of investment banks has shrunk and commoditized.

Historically, raising capital was difficult and public market investors had little awareness of the companies going public. Investment firms were not focused on tech companies. And especially for enterprise startups, retail investors had no exposure or familiarity with them. In this environment, it was the idiosyncrasies of the capital markets that mattered, not the uniqueness of each company. In this model, the company is not that special. Instead, what matters is the standardized process for making the company fit the mold investors expect from an investment asset. Companies may have potential, but they don’t know how to introduce themselves to the investor community in the public markets.

In every marketplace one’s power is proportional to their value added to the transaction. While investment banks view themselves as having an important role in guaranteeing the quality and rigor of which companies are ready to IPO, that seems less true today.1 Banks used to be gatekeepers because markets needed to be told which companies were good. However, discovery is no longer the constraint. Companies are more known and thus the relative leverage and importance of the sell side is falling. And as investment banks increasingly manage only the logistics of the IPO process, they become less important in dictating its terms.

The best founders have figured out that owning their narrative gives them meaningful leverage. Founders and companies can increasingly communicate their narrative in a direct and compounding way to investors. And the roadshow is a progressively smaller component of investors’ views on the company.2 What makes SPACs and Direct Listings notable is not their cost structure, but that they allow companies to much more directly market their IPOs.3

i honestly wrote this entire piece only as a setup for this joke. and i have no regrets.

The ability for companies and public market investors to connect more directly has never been easier. Many of the tech equity funds now do both public market and private pre-IPO investing (and increasingly even earlier stage). Firms like Tiger, Coatue, Durable, and D1—or even T Rowe Price or Fidelity—don’t need to be introduced by bankers to companies. They already have been tracking companies for years and want to know the founders and their companies directly. Founders have the ability to directly build a relationship with the investors that will anchor their IPO. In fact, letting that relationship be primarily mediated by the investment banking process adds friction to the process and is less effective.

Most tech startups are also way better known by the time they go public. This is especially true for consumer startups. Companies like Airbnb, Roblox, Robinhood and Coinbase are widely used and known. When your product is used on a regular basis by investors (or their families) and has been covered extensively by the media, the incremental investor roadshow meeting is less important. Direct daily experience using the product is better marketing than any roadshow presentation. Even non-consumer companies are increasingly well known. By the time companies go public today, they have orders of magnitude more traction than companies going public decades ago did. But also investors just care about tech more. With companies able to IPO at $50B rather than $500M, they are more important and known.

Another characteristic of the current landscape is that the revenue multiples companies can get in the public market have a very wide range. Look at the multiples we’re seeing: everything from 2x to 2000x. This is true both for small SPACs and large direct listings. What separates these companies is how effective they are at conveying a compelling narrative to the public markets.

When the multiple range is so high, the difference between an alright and amazing IPO is a function of people’s belief and confidence in the future potential of business. It can be speculation. It can be based on traction. But also can be on the founders competence in explaining how to think about business today and why that sets it up not just for consistency and predictability but for continual compounding.

As a founder in a world where capital is easy to get, what matters is how to explain yourself, distill the company, and get public markets to understand you in the right way.

Narrative already drives venture fundraising

If this description of the public market sounds familiar, it should.

Where the public markets are heading should be no surprise—it’s what is already done in the early stage venture ecosystem.

In startup fundraising over the last decade, rounds have grown in size, and more importantly, bifurcated into different classes of companies. There are orders of magnitude across the range of valuations for companies with the same level of revenue. Some companies raise at 5x while others can raise at 300x+ ARR multiples. Among pre-revenue companies, the spread of valuations is even greater.

More crucially, in the venture ecosystem, there is universal acknowledgement that founders should drive their fundraising process and pitch directly to investors. A half century ago, companies used to hire bankers to help them raise capital. Today, no VC would take a company doing that seriously.

Being able to best convey the progress and promise of a startup is the job of the CEO. No one has better context on and ability to change the business. And no one is more responsible for conveying that not just during fundraising, but every day—to everyone.

There are three types of fundraising pitches: narrative, inflection, and traction raises:

Narrative pitches are driven by a compelling story of what could be

Inflection pitches are driven by secrets discovered. The company has hit some inflection point that, if investors were astute enough to understand, would make them realize now is the ideal risk-adjusted time to invest

Traction pitches are driven by the results of what’s already been done. The company could be a black box and investors would invest solely off the metrics

the original ngmi. see i am hip with the kidz terminology

The dirty secret is that there is no such thing as traction pitches anymore. Because as every company knows—our best days are always yet to come.

Ironically, the companies with the best traction want to be given credit for their future potential the most. No one wants to rest on the laurels of the past. And achieving the highest multiples requires having a narrative of why even more is to come.

Fundraising and IPOs are natural loci for companies to take a step back and shape their narrative. They are natural points for companies that are often mired in the day-to-day to think hard about their business from a multi-year standpoint. However, while fundraising is a good prompt for companies to think about their narrative,4 the importance of carefully distilling a company’s narrative is increasingly ubiquitous.

there’s a lot going on in this chart. I was told to cut down graphics so i just jammed them all into one gif. malicious compliance.

Narrative leverage in an anomalous world

The more static and predictable the world is, the less narrative matters. Historically most businesses followed clear precedents and fit neatly into paths. If starting a restaurant, the potential range of revenue and costs is known. There are few surprises, so it’s easier to look at the current state of the business and know what it will look like in a few years. There is little volatility.

Tech startups radically break this mold. By definition they will be unrecognizable in five years, whether that’s because they are a unicorn or because they are extinct.

One essence of the tech industry relative to others is the ability of tech companies to precisely select their atomic units and where they sit within their ecosystems, leading to hugely different outcomes.

Empirically, one way to see this is in the widening spread of valuation multiples. Every week, we hear of another company raising at high valuations, but more importantly wild revenue multiples. At the series A and B rounds, we’ve seen multiples of 100x+ or even 200-300x+ ARR become regular occurrences. They’re not common; most companies’ rounds are still raising nowhere near this multiple. But they do exist: there is a subset of companies that are able to raise at orders of magnitude higher revenue multiples. The spread in revenue multiples is widening. Companies with the same amount of revenue increasingly get wildly different valuations. This is the power of narrative, in contextualizing the snapshot of a company’s performance.

There are a number of reasons narrative is becoming more important:

Large dynamic range of outcomes. Startups have a huge range of outcomes. They can be worth nothing and a decade later be worth billions. And this spread is expanding. The largest tech companies are now worth trillions. More topically, over the last decade the distribution of outcomes for most tech IPOs has increased by an order of magnitude. Enterprise investors, for example, used to assume that beyond the once-in-a-generation company, most enterprise IPOs were hard capped at single digit billions in market cap. The entire business model of enterprise venture investing was built on this assumption. And it is no longer true.5 When the potential range of outcomes of companies has many orders of magnitudes within it, then one’s confidence level in the probability distribution of outcomes becomes incredibly important.

Back-weighted LTV. Increasingly tech companies don’t make the majority of their revenue from the first interaction with customers. In each sector this is done via a different approach, but fundamentally SaaS, freemium, Open Source, etc are all examples of this. This is one of largest trends in tech over the last few decades and is worth further exploration*. Revenue being a lagging metric isn’t bad, but it means that understanding the value of a company requires a rigorous understanding of the leading metrics that will drive future revenue. This again means that a company’s ability to explain to others how to think about the business and why they are so confident in the inevitability of future revenue based on current product metrics is crucial.

Sequencing to Multi-Product / Platform. With enough scale, there is a truth about modern public tech companies: you either die a single product company, or live long enough to be multi-product or a platform. This is the inevitable path for almost every successful company, but the likelihood of success is hard to tell while the company has a single product and has never tried to make the leap to multi-product or platform. The best companies get valuation multiples that give them credit in advance for future business model sequencing This again puts the onus on the company to explain why they can become multi-product and what it will mean.

Compounding loops. Finally, we are still very early in our understanding of how to quantify and predict the returns of compounding loops. Network effects, economies of scale, and still unnamed types of loops all can have a very disproportionate impact on long term value of a company—but there is no simple way to infer it from an early snapshot of performance. Companies must work on explaining the compounding loops they are building, what leading metrics to look at to see their potential, and why they will be so powerful.

Self-fulfilling prophecies: When is narrative justified

Narrative leverage in tech is most commonly understood in the sense of Steve Job’s Reality Distortion field.

Personally, I like to think of this narrative leverage as a form of PE ratio (Price to Earnings ratio). I sometimes call it the PR ratio (Perception to Reality ratio).

How do we know if narrative leverage is good? It’s easy to think of many companies where the reality of the company didn’t live up to the hype. Some of these were fraudulent and illegal, like Theranos. But tougher are the ones that lie somewhere on the spectrum of over promising. There’s a blurry line between the need to project confidence in order to gather all the resources to make the hype a reality and lying about things that will never happen. And while there’s no perfect way to separate these, how should one think about that spectrum and about the appropriate amount of narrative leverage a company should have?

It’s also important to note that narrative is not just stories founders make up isolated from reality. At their best they are distilling for outsiders truths already known internally. These can be explaining the leading cohort metrics or early signs of TAM expansion potential that give confidence.

Here is where I think the analogy to PE ratios is useful.

In the public markets, the PE ratio of a stock is the ratio between its market cap and earnings. This is a reflection of how high investors will value a company relative to its current earnings.

If a company’s value is the net present value of future cash flows, its PE ratio in a rough sense is a proxy for how confident investors are of high future cash flows.This is a simplification, but you can generally view a company with much higher PE ratio than another company with the same earnings as one investors think will have higher growth and future cash flows. Over time the rate of Earnings growth will help catch up to the expectations, bringing the ratio down—or investors will continue to believe, keeping the ratio high.

When we talk about revenue multiples of startup funding rounds, this is the private market equivalent of PE ratio.

What is the benefit of a high PE ratio? It is cheap cost of capital. It allows companies to raise capital with the benefit of getting credit for what they will be in the future. It is a loan pulled forward from the future.

Is a high PE ratio good? The answer is not a simple yes.

A PE ratio is good if there is appropriately high ROIC (return on invested capital) by their usage of it. If getting a loan on a future promise allows you to deploy it effectively to better live up to those aspirations, then it was not just worth it—the aspirational perception helped catalyze and make its own prediction inevitable.

That is some kind of magic, creating something from nothing.6 An ouroboros eating only itself yet somehow growing. Perhaps modern time travel is our ability to take a loan out from our future success to ensure we achieve it.

PE ratios are a promise continually renewed—and they can be warranted or misplaced. When companies’ earnings cannot keep pace and live up to these expectations, we see the price and PE ratio eventually fall to reflect this, even more so where companies don’t have the ability to take advantage of their PE ratio and the lofty expectations of them to improve the business now.

Outright frauds like Theranos cannot live up to their valuations. Their PE ratios are bad since with or without the benefit of a high multiple, they can never grow into their valuation.

More complicated are companies like Tesla. For years there were vicious debates over whether Tesla was over or undervalued, with vitriolic takes from both sides. What made the question hard to answer was that they were both right. Elon takes on industries where new approaches can work as the industry cost curve improves, but require massive and cheap access to capital for extended durations to work. Elon is not unique in this dynamic. It can also be seen in fields like AI research.

Thus Tesla’s PE ratio is in many ways self-fulfilling. If Tesla could get people to extend the access to capital it needs for long enough it will be successful. If it could not, then it would have collapsed. Ironically, this means that far from Elon’s antics being distracting, his ability to maintain these high PE ratios might be the most important driver of the company’s ability to succeed.

But this general concept is not unique to the public markets, or to money. In some sense, even people have a social capital PE ratio. PE ratios in the public markets are just one instance of a more general concept of having some view of what something can become—and giving them today the benefit of that future tomorrow accordingly.

Narrative leverage is the PE ratio of a company. Not just for cheaper cost of future capital, but also for everything else companies care about too. Cheaper cost of recruiting, customer development, and perhaps most importantly—internal coordination.

Venture as social staking: the future is founders

Modern venture itself is not just about money and the cost of capital. Most founders would give a discount in pricing to the top VC firms. What the top VC firms are selling today isn’t money—they’re lending their own brand to startups. Having Sequoia invest will lend the stored PE ratio of Sequoia to the portfolio company. This will help give them a cheaper cost of capital, recruiting, and customer acquisition.

LPs may care that a firm has good returns, but that’s not intrinsically relevant to founders. It only matters insofar as those returns translate to stronger brand value or direct relationships that can be used on behalf of the founder’s company. This is why venture today exhibits power laws with the top firms attracting disproportionate returns.

In today’s ecosystem, however, companies are increasingly able to have as much, if not higher, narrative leverage than VC firms. The top companies—and especially their founders—are more known than their VCs. At the extreme end, Patrick Collison has much more ability to attract investment, customers, and hires than any of the VCs on his cap table. Every year there’s an increasing number of founders at each stage who have higher brand leverage than what VCs can bring to the table. This is both due to the growing primacy of founders as well as the relative stagnation venture has had beyond brand network effects.

employees is on this chart. oh you can’t see it. oh…how weird.

And founders have so much more surface area to compound this brand leverage than their investors can. Founders can uniquely refine their narrative hand in hand with building the business to make it best resonate with all their prospective investors, hires, or customers. They also have the full resources of their company to bring that narrative to bear.

Narrative distillation is a core part of company building

The largest trend in every function within companies is that they’re being pulled internal. Engineering was the first. The birth of modern software companies began when companies first understood that engineering wasn’t a back office job to outsource, but a core part of the primary job of a company. Core, not commodity.

Endogenous compounding is increasingly the foundation of all modern successful companies. In a world where it is hard to be successful and unknown, all external channels increasingly get arbitraged. Companies that discover some novel market or promising acquisition channel quickly find themselves joined by many competitors. And the outsized returns they briefly got fall back down to earth under the weight of competition. It is internally compounding advantages that fight the gravity of this reversion to the mean. This is why we talk so often about network effects & economies of scale. Because like any polynomial equation, as scale rises & approaches infinity, only the highest order bit matters. And it is the aspects of the company that are internal to its organization or ecosystem that can most compound unimpeded by the outside world.

While engineering was first, it is not unique. Every function whose returns on iteration are high and non-commodity will follow the same path.

The transition from marketing to growth was this exact same process. Traditionally marketing was something done after the work on the product was already complete. Companies would finish the product and throw it over the fence to the marketing team. The easiest way to know if a function is core or commodity is 1) whether the function is identical at other companies, or unique to the particulars of their company and 2) whether it has feedback loops in the company or purely uses external channels.

Modern growth teams are impossible to remove from the core flow of their companies. In fact, they are fused to core product and engineering. How can you do growth without it being inextricably tied to the core flows of the product?

Brand marketing is still important, but on a relative basis it is increasingly shrinking compared to paid acquisition and more importantly core product driven distribution. If you think about bottoms up, product driven SaaS companies or viral social networks, they are examples of how impossible it is for traditional marketing to compete with the product itself. The best companies understand that distribution is a first party concern when thinking about a product, not some checkbox to finish after.

In “Why Figma Wins” I wrote about how design is undergoing this exact same transition. Design at the best companies cannot be relegated to artists told what to make after all the decisions have been made. They must be part of the core decision making throughout the entire process and all its iterations. This doesn’t just fall on the companies. It also means designers must accept more responsibility. The best designers want to be at the table. And they understand that they must not just think at a creative level, but also in how their design process and output shapes the core business. The best designers not only do this, they relish it.

The same is happening to the narrative of companies. Increasingly, narrative isn’t primarily about external framing. It’s not something done after the work has been completed.

Adobe has continually shown over the last few decades how core managing the narrative is to getting the support and coordination of investors and employees as the company makes fundamental shifts to their business model. Whether that be in adding new products, transitioning to the faster internal cadence of a SaaS company, refactoring into a cloud-first infrastructure and pricing model, or the myriad other endeavors Adobe has undergone from building printing software to the full expanse it is now.

Those shaping the narrative must intimately understand how employees, investors, and customers think about the company. Refining and expanding the narrative is entwined with the company’s progress. Narrative is shaped by each iteration of a company’s processes and products. And in turn a company’s evolving narrative shapes how it focuses its processes and builds its products.

Founders are responsible for holistic narrative distillation

Too often we focus on how much money a company can raise. But money is rarely an ends. Instead, it’s a resource to spend to functionally derisk the company. Historically, capital was the scarcest resource. Venture capital as an industry was built and structured around capital scarcity as the most important blocker on company success.

But increasingly it isn’t scarce anymore. And it certainly isn’t the main blocker for many of the top companies. Talk to top tech companies today and raising capital is ironically one of the easier aspects of building and derisking the company. Hiring and retaining a talented team is far harder. Acquiring and retaining customers is harder. Understanding and getting the team coordinated on what to build is harder. Oh, and did I mention that hiring and retaining a talented team is far harder?

This is the CEO’s job: to raise and allocate the capital needed, but also to build a team capable of building the product needed and getting distribution. All while understanding what the company needs to build and helping the team understand and orient around it.

Narrative leverage is not just an advantage on the cost of financial capital. And not just a PE ratio with the financial markets. It exists in the leverage with all stakeholders both external and internal. It’s what makes prospective employees excited to apply and work for your company—despite all the tech companies fighting for talent. It’s what gives your customer confidence you will not only not go under—you’ll be focused on building a product that’ll continue to blow them away.

And perhaps most importantly, it’s what makes the team understand not just what the company looks like today—but what it could look like in five years. And makes employees able to see beyond their role, to how they fit into the larger picture of the company’s strategy.

Who’s in charge of that narrative? The answer is complicated and different depending on the audience.

From the employees’ perspective, it’s internal comms. From the customers’ perspective, it’s marketing—or perhaps the product itself. From the investors’ perspective, it’s investor relations.

i buy loops in bulk now.

But at most companies, these are primarily teams who manage how the narrative is distributed and shared. They are rarely the ones shaping and iterating on it, especially where it must bend the direction of the company itself.

There is no team that owns the narrative of a company. No team that determines its atomic concepts. This is why we often see large disagreements within a company on how to think about itself.

Some of these differences are natural. After all, customers care about different aspects of a company than its investors. And employees in different roles may have good reason to be focused on different timescales. But too often, the disagreement is unintended and harmful.

At most companies, only the CEO or founders can shape and reshape narrative.

Top companies already recognize primacy founder led narrative

Suggesting CEOs should prioritize this narrative distillation and go direct to their audiences isn’t idle prognosticating. The top CEOs already do care, and spend significant time on it.

The company that was first and best at building their brand is Stripe. There may be no company with higher narrative leverage than Stripe and the Collison brothers. From its earliest days, Stripe has excelled at this.

Stripe has long since grown into much more. But in its early days a significant amount of its value was simply in its ability to get great engineers to work on payment integrations and internationalization. Today, working on developer-first API companies may be sought after, but that did not used to be true. If a company tried to get its best engineers to work on internationalization of payments, they’d just refuse. Or quit. Stripe was able to get great engineers to work on these distinctly not high profile areas. And that alone, is worth a lot.

It’s not that the Collison brothers set out with some deliberate master plan to build a brand, culture, or personal reputation that would attract developers to work on Stripe. More likely, is that they filled a structural hole around payments. Payments needed a company that was developer first and engineering driven, and only founders with the predispositions of the Collisons could attract and build that kind of team in a space that those engineers would have otherwise dismissed.7

KK Note: Even today, the ability to get strong engineers to work on a problem engineers normally don’t want to work on remains a very strong formula for returns.

The Collison brothers may not have started with narrative in mind. But they have been quick to understand and capitalize on it. Stripe’s brand leverage among prospective employees in tech is incredibly high.

Stripe’s slogan, “Increase the GDP of the internet” points at a far loftier vision and more ambitious goal than the mundanity of payment processing. And this is reinforced in both much of Patrick Collison’s projects outside of Stripe as well as initiatives like Stripe Press.

And if Twitter is an increasingly strong channel for hiring and customer acquisition of tech startup customers, Stripe is the most dominant brand among tech Twitter. So much so that there appears to be an entire genre of Twitter content that is new Stripe employees tweeting about their onboarding experience.

You can increasingly see other top companies shifting to invest more in their company and founder brands. Shopify and its CEO, Tobi Lutke, are a good example of this.

In the last few years Tobi has become much more visible publicly. He goes on podcasts, hangs out in Clubhouse, does AMAs while streaming videogames on the Internet, and much more. If allocation of attention is the best proxy for prioritization, Tobi has strongly signaled his view of the importance of building personal brand and shaping Shopify’s narrative.

Increasing brand awareness and expanding the CEOs’ reach is real leverage. Reinforcing that Shopify is a tech company doesn’t hurt their multiple in the public markets, but cheap cost of capital is likely not what limits Shopify. Like all tech companies of this scale and success, their ever present constraint is recruiting. Having a strong brand and easy access to capital helps, but all their competition have that as well. The red queen race for talent is unceasing. Especially as Shopify has expanded its executive hiring outside of Canada to the US where it is relatively less known.

Founders have a unique ability to build brand for their companies. But of course companies must build it beyond them. Shopify has many other initiatives, like a studio producing TV shows and movies on entrepreneurship and starting an esports team.

Shopify is not alone. Spotify is now making podcasts about how they build their product, and Daniel Ek is doing interviews on podcasts and blogs. Twilio is launching a magazine for their customers. And of course Elon is…being Elon.

It’s an advantage today. And will be table stakes tomorrow.

Final thoughts

Narrative is the other side of the coin of functional derisking. If a company is a series of functional derisking loops, then narrative is the leading edge of what is to come.

my editor told me no one would understand this chart. so it’s for me, not you.

Founders want credit not just for what they have already done, but what they are going to do: launching new product lines, changing their business model, becoming a platform. They want to pull forward credit for these future developments to the present to help make them inevitable.

Even more so, they want their team to have synchronicity around what is most important for the company’s future and how to prioritize and make tradeoffs.

What’s the difference between future investors and potential hires thinking a company is distracted and unfocused versus inevitable and defining? It’s in the coherence of the company’s logic for each sequencing of steps and how legible that narrative is made to them.

And in today’s market it is increasingly the founders who are able to distill and manage the overall narrative. This is only increasingly as companies undergo significant business model changes as they scale and the capital markets treat startups more as a fungible asset class.

Product market fit is just narrative distillation for customers. It only makes sense that this same process is as crucial for investors and employees, too. And just as we have spent so many years reinforcing the primacy of founders focusing on product market fit—and the process of how companies converge on it—so too must founders take distilling their narratives for all audiences equally seriously.

Appendix: Making companies that matter

Recently8 I tweeted that I was glad to see Discord hadn’t sold and that there’s some list of companies I hope never sell. While I do think it would have been underpriced, this isn’t the reason I don’t want them to sell.

Companies like Discord are not important because of the returns they may have. There is no shortage of companies that can drive returns. There are far fewer that can change their industries. And Discord is not alone—there is an entire rising generation of companies this applies to. Companies like Figma, Canva, Flexport, Benchling, and others are all at the cusp of getting to meaningful scale within their industries. (KK note: I don’t think I need to worry about any of them selling. But yes if you are a founder of any of these companies please don’t sell).

In prior essays I wrote on how we should judge venture firms not on their returns but on the value they added above replacement to companies. This is true for companies as well. Companies should be evaluated on the value they add above replacement.

Many companies simply occupy a structural hole in the market. In a world where they did not exist, some other company would simply have occupied their slot, without loss of generality. These companies may have significant profits, but they don’t matter. In some sense the profits were going to be realized regardless, and should not be attributed to their contribution. Great companies pull forward the future. They introduce solutions or business models that would otherwise take many more years to come about.

And the most defining companies change their industries’ trajectories and hurtle their ecosystems into shapes that otherwise wouldn’t have been seen at all.

There are only a few dozen companies at a time that have line of sight to being defining companies in their industry. While correlated to profitability, this isn’t about their ability to generate money. It’s about the gravitational force they will exert, re-orienting their industry into a new structure and alignment and proving out new business models whose structure will be replicated by all companies to follow.

This is the most compelling narrative that a founder can create around their company: that they have bigger ambitions than just succeeding as a business, that they have a chance to change the nature of business itself. For a select few, it’s not just a pipe dream—it’s the truth.

Endnotes

[1]: The current public markets are like a bar, and the investment banks are the bartender trying to regulate how many IPOs get served. But investors don’t want to be held back from more IPOs, whether they have had too many or too few drinks. And at this point investment banks have given up on trying to regulate this. Whether investors have had one drink, or one too many drinks, is an exercise left to the reader. Or rather how leveraged long tech beta the reader is.

[2]: If we are mutuals and you are planning to IPO soon. First, congrats. Second, please let me convince you to not let the investment banks run your IPO process the traditional way.

[3]: Direct listings have financial benefits relative to traditional IPOs, but I think these are secondary. And for example, modern DPOs seem to shift who gets the preferential pricing from the investment bank’s clients to a friendly hybrid fund that gets the pre-IPO floor setting round. This is a positive shift, but more incremental than transformational. It is the shift to companies owning their own narrative and marketing that is overlooked but most important.

[4]: Ironically, the hotter and more founder friendly the fundraising environment is, the less it is a fitness function forcing narrative clarity from founders. For many founders lucky enough to have VCs throwing money at them, there is no longer anyone but themselves who can force them to really refine their narrative.

[5]: Over a long period of time, the form of the venture industry is dictated by the scale, expected value, and risk distribution of the ecosystem of startups. If that distribution shifts, so too will the venture industry.

[6]: No, seriously. That is true magic.

[7]: Paul Graham has a great essay about schlep blindness. In it he posits that the reason we see founders avoid building companies addressing schlep problems is an unconscious avoidance of unpleasant work. This may be true, but I suspect the larger reason is that we don’t value solving these schleps appropriately. Historically the social capital in working on these areas was far less than on public facing products. Which made it hard not just to get excited about personally working on them, but also to hire teams and bring on investors. The best solution then is not ignorance as Paul Graham suggests, but rather a collective reappraisal of schlep industries. Which seems like what has happened over the last decade, as areas like b2b SaaS have become desirable. Also suspect the bigger macro driver is demand side fragmentation and growth. But shhh.

[8]: Given how long ago I started this essay “recently” is no longer accurate.

Acknowledgements

Many thanks to Keila Fong for all the help editing this piece.

Additionally, thanks to Kane Hsieh for advanced gif manufacturing assistance.

All graphics in this piece were created with Procreate and Figma. An integration between these two might have a target audience of only me. But I would love it. Many many thanks to Rogie for creating this amazing Procreate Import for Figma plugin. I’ve been very excited to take it for a spin, and it is life changing. Being able to import all the layers of a procreate file into Figma allows for so many more powerful combinations of the two tools. If you read my blog you don’t need me to repeat my love for Figma and what its plugin ecosystem enables. But this really is a perfect example to me of the power of Figma’s plugins—and even more so its community. Also, the power of twitter. heh.

Edit: Thanks to Nitesh for keeping me accountable on holding the line against title case hyperinflation

* Further pieces to be written on these subjects**

**I’m probably lying about this. To you, but mostly to myself.

Algorithmic Design, Tinder, and Platform Governance

And a bunch of other random stuff

I’d pretend we’re doing it because people say our posts are too long. But I checked the word count of the transcript, and it was 15k words which is significantly longer than most of my posts. So I guess you won’t really be saving much time.

We’re hoping to go into more follow up discussions on many of the topics we write about. As well as have some guests on.

Fear not, I’m not shifting away from writing. In fact, have been editing a new post I’m hoping to publish soon. It just turns out this is coming first because…video is a lot easier than writing. At least the way we are doing it with no second takes. We’ll see when I can publish. The process of making videos has also been fascinating. Whether here or on Twitter, I’m guessing will have some post-mortems on many parts of that process to share.

How Figma and Canva are taking on Adobe—and winning

In 2010, Photoshop was ubiquitous. Whether you were editing a photo, making a poster, or designing a website, it happened in Photoshop.

Today, Adobe looks incredibly strong. They’ve had spectacular stock performance, thanks to clear-eyed management who’ve made bold bets that have paid off. Their transition to SaaS has been seamless, for which the public markets have rewarded them handsomely. And they’re historically one of the best companies at M&A; their product lineup is a testament to their ability to acquire new product lines and integrate them well into their multi-product ecosystem. Perhaps most importantly and least appreciated, they have dramatically sped up the cadence of their internal product development process and feedback loop. Like Microsoft, they have successfully shifted from a legacy company operating on an annual (or longer) release schedule to a truly cloud company shipping updates at a sub-weekly pace.

Nevertheless, there are a few segments of design where they’re no longer the market leader. Companies like Figma, Sketch, and Canva are examples of products that have been able to become top products despite Adobe’s ubiquity in all things design. Figma showed up in Adobe’s annual report for the first time in 2019. They reprised in 2020, and I’m not uncertain they will continue to be in it going forward.

How should we understand these market transitions and why these young companies are able to thrive, even against a strong incumbent like Adobe?

These companies have distinct atomic concepts from Adobe. The primitives that their products are built around are fundamentally different from those of Adobe’s product lineup. It’s these different fundamental atomic concepts that turn Adobe’s advantage of an established product and existing userbase into a weakness that hinders their ability to counter these upstarts. The opportunity for these new atomic concepts to thrive is driven by the new use cases and types of users unearthed during market transitions.

Understanding the phases of market transition and what drives them is a universal process worth examining.

New use cases: designing for digital

For most markets, there are advantages to being an incumbent. Markets converge as companies arrive at the preference frontier of customers. This leaves little potential energy for new startups to take advantage of.

Market entropy is good for new entrants.

It’s not impossible to break into a market by brute force, but it’s hard. Very hard. Most successful companies, especially startups, have found tailwinds to harness that help pull them forward.

Changing customer needs are the largest source of entropy in markets. When customer needs rapidly change, there is less advantage in being an incumbent. Instead, legacy companies are left with all the overhead and a product that no longer is what customers want.

There are many causes of changing customer needs. Often there are new and growing segments of customers with different use cases. Existing products may work for them, but they aren’t ideal. The features they care about and how they value them are very different from the customers the legacy company is used to. Companies resist changing core parts of their product for every new use case since it’s costly in work, money, and attention. But every once in a while, what was once a small use case grows into one large enough to support its own company.

Other times the scale or dynamics of a market shift enough to make a product no longer work despite having been a great fit. Companies are often caught flat-footed by these situations because what they have done successfully for years suddenly starts to falter—and they aren’t sure why. Ebay is a good example of this. Their decentralized auction model was very good in a nascent internet economy when there was a scarcity of items being sold online. Once ecommerce became commonplace, price and speed became much more important factors and Ebay’s decentralized model was at a disadvantage. Amazon was much better at building economies of scale in this post-liquidity ecosystem.

Another source is when the customers themselves change. Often the function of a tool remains the same, but the type of user changes. These new types of customers often have different things they care about and resulting product needs.

The internet drove entirely new design use cases. Photoshop was built for editing photos and images. It’s a powerful tool that operates at the pixel level. However, many of these new uses weren’t about image manipulation. Images were a component—not the essence—of the job users were trying to accomplish.

For some users, this was designing digital products. Designers at software companies or any company with a website wanted to create the websites and software products they worked on. This is less about image manipulation and more about designing the UI and UX of these digital products. Vectors are more important than raster graphics. The complexity and process of designing these high-value designs also got increasingly more sophisticated. These designers worked with teams of other designers and non-designers. Their designs are part of a larger product development process and what mattered wasn’t just making a design, but how that the entire process could be improved to make collaboration easier and handoff of designs better. Iteratively.

The complexity of the designs and the components in the resulting code became more complex, too. The need for their tools to have a higher-level understanding of the components and variants became more important. It’s increasingly useful for designs to understand the same concepts and abstraction levels as the HTML and CSS in the resulting end product.

For some users, this was designing content for social platforms, digital ads, or even wedding invitations. These were often made in Photoshop, but again, pixels are the wrong abstraction level. Images are not the sole component; they are just past of a larger design that includes graphics, text, and more. Similarly, the customers are very different. Many of the people now doing what is, in essence, design work don’t think of themselves as designers. They just have a very specific thing they want to create, with the least friction possible.

The internet dramatically scales up the volume and type of new use cases for design. In many ways, this helps Adobe. With platforms like Instagram, the number of people editing photos has expanded by many orders of magnitude. While editing on platforms like Instagram may have increased significantly, Adobe has been a huge beneficiary of the internet and the shift to cloud—and their stock price is a testament to this.

[KK Note: Platforms like Instagram strapping editors onto their social platforms and eating into Lightroom from the bottom up is well worth its own discussion. And perhaps someone will convince Mike Krieger to do the definitive piece on that.]

Software may be eating the world. But it’s also building new worlds? I’m going to need a refresher on remembering the Andreessen Horowitz talking points

This is even more true in video. There are orders of magnitude more video creators as the ability to record video has become ubiquitous and the platforms where video is the default format have grown. Even more striking, many of the dominant video platforms—like Youtube—are purely distribution focused. They don’t even have any editing capabilities. Instead, companies like Adobe end up being large beneficiaries of this need.

[KK Note: Platforms like Youtube still having not built any semblance of an editor into their platform is *also* well worth its own discussion. I’d say we’ll never know what could be, but then I look at TikTok and all is right with the world.]

But Adobe hasn’t captured it all. And in many of these new emergent use cases and customer types, Adobe has lost the lead to new startups.

Tapping into the right level of abstraction

The best products map to how customers think about their workflow. They match the abstraction level of their customers: not too high that it’s unusable, but not too low that it’s hard to use easily or extend in more complex ways.

They choose the right atomic concepts.

These are the core concepts around which the entire product is built. They not only align with how customers think of their workflow, but often crystallizes for customers how they ought to. Great atomic concepts are honed and then extended and built upon in more complex compounds that…well for lack of a better word…compound.

Similar companies often have slightly different atomic concepts that end up making them meaningfully distinct. Photoshop is focused on pixels and images. Its focus is on editing images and pictures. And its functions operate by transforming them on a pixel level.

Illustrator is similar, but it operates on vectors, not pixels. This is a higher level abstraction. Neither is better or worse, they are just more suited to different use cases. Photoshop is better for modifying images, while illustrator is built for designs where scale-free vectors are best.

Sketch, like Illustrator, is vector based. But is designed for building digital products which means things like operating at a project level. It is not individual designs, but crafting entire products and user interfaces—and the needs for repeatability and consistency inherent to that.

Figma builds on Sketch’s approach, but also includes a greater focus on not just projects but the entire collaborative process as the relevant scope. Similarly, it also treats higher level abstractions like plugins, community, and more as equally important concepts.

Canva is similar to Photoshop and Illustrator, but its users aren’t designers who care about low level tools. Instead Canva’s core atomic concepts are around the different templates and components to help them easily accomplish the job they are doing. And the designs they are working on are not quite at the project level of making a digital product. They are canvases that include images and design.

There are many more axes, but they don’t fit in this stupid 2D chart

Atomic concepts are fundamentally linked to the core loops of a company. Expanding or changing these loops often involves adding to a company’s vocabulary of atomic concepts or adding them together in more complex ways.

Emergent use cases and new customer types lead to new ideal atomic concepts. These new workflows and different customers have different priorities than existing customers. How they think about their problems and weight possible solutions is different, even if often the end output has similarities. Of course, astute readers will pick up that causality is reversed here. New types of customers are a good proxy for where to pay attention. But it is actually the changed atomic concepts that are what make startups a compelling contender against incumbents in the space.

Customers don’t care about your technical architecture or internal org structure. When these no longer align with the job they are trying to do, then all the sprawl of the company becomes harmful, not helpful. These are the core bedrock that are much more difficult for a company to change mid-flight. Everything that makes an established company strong is built on top of this foundation and will fight back against changing them. Take Blockbuster and its reliance on physical stores and late fees. People often fall into the easy narrative that incumbents are asleep at the wheel. That they are too stupid to see the coming threat. This can be true but it isn’t the most common reason. Contrary to popular belief, many execs at Blockbuster not only saw the threat Netflix posed, but also the opportunity for Blockbuster to have claimed the mantle Netflix now holds. They even spun up a team to take Netflix head on. But what made retail stores and late fees so powerful and profitable for Blockbuster is also what made them so hard to displace. Every move to prepare Blockbuster’s core for a digital future was resisted by execs who generated more revenue, store operators who were livid at being cut out, and Wall Street investors uncomfortable with turning a consistent business into a high risk venture.

Rare is the company that can change its core atomic concepts. It’s why companies like Amazon are so impressive and so daunting. Startups thrive by finding asymmetric angles on incumbents that they are unable to follow. What is safe from a company with no sacred cows?

Understanding the core abstraction levels of a company is hard to understand from a distance. Which is why looking for emergent customer types with different needs is a useful substitute.

Figma bet on collaborative product design

Sketch was the company to first understand the market opportunity in designing digital products. Launched in 2010, Sketch was built entirely for designing the UI and UX of these products. Its atomic concepts were those best for digital products: vectors and projects. These were also what made it hard for Adobe to compete with their pre-existing product line.

In a classic innovator’s dilemma, Sketch’s best feature against Adobe was that it dropped everything that wasn’t best for making digital products. This allowed it to focus only on creating the best experience for vector-based digital design. Unlike Photoshop, it was vector based. And unlike Illustrator it was built with larger complex projects as the focus rather than specific isolated designs.

In retrospect, Sketch stopped at a half measure. Designers creating digital products did need vector-based design tools. And Sketch also understood that they were working on more complex projects vs one off designs that needed better project-first features. But these designers were also often working on teams—both with other designers and, more importantly, with non-designers. They weren’t designing in isolation, but as part of a larger process.

Sketch, like Adobe before it, lacked in this area. Everything from Sketch’s technical architecture and desktop based product to its pricing model and platform structure were a poor fit for this collaboration. The demand for these features could be seen in the messy ways that companies hacked together solutions to this and the many products that sprung up to fill these holes. Companies like Zeplin, Sympli, and Invision grew out of designers’ needs for better ways to coordinate with the other designers, PMs, and engineers they worked with. Sketch’s plugin system, like Adobe’s, felt more bolted on than core to the platform.

When Figma first started, it was more directly a Photoshop competitor. Over its first two years, though, they shifted their focus specifically to designers working on the UI and UX of digital products as they talked to more potential users. Building out the product to enable collaboration uniquely was key to these designers. Doing this was non-trivial. The technical challenges to do so were very hard, though Figma was well set up due to Evan Wallace’s technical prowess and specific knowledge in new technologies like WebGL. Building for collaboration to its fullest extent has led Figma to rethink almost all of the company—leading to new pricing models, distribution models, and sharing form factors.

For those interested in reading more on Figma, I have a prior post that can be found here so will avoid rehashing many of the same observations. Figma’s success came as it honed in on this growing use case of complex digital products built by larger teams of designers and non-designers—and in finding the atomic concepts that were uniquely needed for this new skew of users.

As discussed in Why Figma Wins, over the last few years this is most visible in their expansion into larger enterprise customers. Large companies have the same (if not greater) need for design tools that are built for the collaboration in their org as small startups or smaller teams within them. However, the set of features and tools they need around this look very different from a small team. When Figma started, it found its fit first with small teams, but as entire large companies started to look at it seriously it needed to understand how to think about collaboration and building a design tool not just at a team level—but at the scale of an entire company.

Canva bet on marketing design by non-designers

With the rise of digital platforms like Facebook, Instagram, and Youtube, marketing and advertising have increasingly shifted online. Online advertising has many differences from traditional advertising. Most notably, it is much faster paced—and often more targeted. Companies now do many small variations on the same campaign: testing which versions do best, making personalized versions for different customer cohorts, and adjusting them to the different required form factors of each ad platform. The traditional process of having a few large campaigns each year looks increasingly archaic. The cadence was a function of the primary channels being areas like TV and print, where campaigns are costly so only a few large campaigns can be run a year. As the channels shift, the campaigns, tools, and teams adjust to match the new dynamics.

The fast and the furious

Increasingly, marketing teams don’t need whole design teams working on each campaign. Rather, they want tools that made it easy for them to adjust their marketing designs in small ways—like being able to format it for both their instagram ad as well as their Youtube banner. The background of the person needed to do this changes, too. Instead of hiring design agencies, companies bring this work in house, both because more of the work can be done by non-designers and because the pace of iterations makes working with an external agency too slow.

Once again I am asking you to be impressed by my multimedia use of graphics, drawings, and logos

Marketers and people posting on Instagram don’t think of the design work they want to do in terms of pixels. It’s the wrong abstraction level. They aren’t trying to directly edit the photos themselves. The photos are just an aspect of the specific goal they have in mind. They think of it in terms of the aesthetics and purpose of the design—not just the images but also the text and graphics and more.

Photoshop can do everything they want, but it is too low level. Photoshop’s atomic concepts are images and pixels. Editing at the pixel level is perfect for photos and image manipulation. Canva operates at a higher abstraction level—the one its users care about. Canva designs start with their purpose in mind, whether that’s designing a pitch deck, an Instagram post, or a wedding invitation. Canva has templates and layouts built for that specific purpose, while making it easy for users to add their own creativity, whether by putting in their own photos or using any of the many graphics and components made by the community.

This need is even more felt by SMBs and teams who can’t have a full design team work on every project. Canva’s lightweight editing with easy templates and process for making many small changes like formatting for different social platforms made it ideal for these customers.

This also allows Canva to extend its platform around these molecular levels. Canva’s distribution is driven in large part by their SEO. Unsurprisingly, the very same use cases people use Canva for are what people looking for design tools want to do and search Google for. With their product and templates built around these use cases, it’s easy for Canva to expose that externally and have lots of templates and examples ready to go for potential new users looking to do a specific design. Everything about their user acquisition and onboarding is built around the specific use cases people have and Canva’s atomic concepts. They are built around the functional workflows people have, whether that’s making a Twitter background photo, a wedding invite, or a keynote presentation. And Canva is committed to making that as easy as possible.

There is something very illuminati about this pyramid and sun. You heard it here first

Defensibility through becoming a platform

As they’ve grown, Canva has expanded their ecosystem by creating marketplaces and communities around templates, layouts, fonts, and more. Most users don’t want to build from scratch. With Canva’s marketplaces there is an entire ecosystem of pre-built components they can use, both free and paid.

Canva having this strong ecosystem of add-ons is very powerful. Add-ons allow Canva to address the huge scale and varied needs of all its customers, far more than one company could ever do on its own. This makes it possible for each customer to use Canva in a way that will be personalized for exactly the use case and aesthetic they care about.

I did not repurpose the first chart. No one will believe you. shhhhhThere is nothing sadder than the fact that no one will build a Procreate x Figma integration JUST. FOR. ME.

Creating free and paid add-ons have long been a staple for most design tools. However, they haven’t been tightly integrated into the product, adding friction for users. In contrast, Canva builds add-ons seamlessly and directly into the product, making it easy for users to access them directly and leading to higher usage. Treating these marketplaces as first parties has a number of additional benefits. Beyond increasing the value of the product, it also cements platform network effects for Canva. A growing community of creators monetizes by selling add-ons for Canva; this reinforces Canva as the tool to use with the most robust ecosystem.

There is entire category of ecosystem loops that no one seems to talk about. Ecosystem loops deserve love too

This is just one example of how companies can use platform network effects to extend and defend their beachhead. There are few sources of defensibility stronger than the cross-side network effects of platforms. It makes it hard for any new competitors to get traction. Without a large enough user base, a new platform can’t attract developers to build on top of it. As a result, new competitors also lack the ecosystem of add-ons to meet all the needs of and attract users. This is why platforms are so enduring. They allow companies to scale the needs they meet beyond what’s possible for a single company and they create chicken and egg problems for any competitor hoping to follow.

Extending this playbook to other spaces

Design isn’t unique among fields. All these same factors that are driving new and large use cases in demand are similarly arriving in most fields, especially in all forms of digital content. It’s inevitable we will see many of these same changes happen to video as they have in design and photography, though the specific use cases and needs that emerge will look different.

The most active area obviously undergoing this market transition right now is the broader productivity space. Over the last few years, many of these new companies (Airtable, Notion, Coda, Roam, Retool, Webflow, and Loom, to name a few) have seen remarkable early traction. But it’s also hard to delineate what the exact spaces are within productivity and collaboration and which companies cluster together in which buckets. Many of the companies have lots of product roadmap overlap as they each navigate the amorphous high-dimensional space of customer types and needs.

Even for those companies with early success, many have yet to crisply define the atomic concepts they’re betting on and to position themselves accordingly. Which are competitors with which? Who are their customers and which use cases will be the most important workflows to build around? What factors will determine which companies succeed and centralize their markets?

Companies have trouble navigating these questions because customers themselves don’t think precisely about what they really want. These companies have the opportunity to change how customers think about their own workflows. The best companies introduce better atomic concepts and help push their customers forward. Strong enough products will have ecosystems around them whether or not the companies actively manage it. The best companies don’t just benefit from these ecosystems, they build their platforms to enable and direct these ecosystems in ways that empower their customers more.

Figma is beginning to expand its scope with new initiatives like plugins and communities. These are not the only ones I expect we’ll see (and there’s one that I’m particularly excited to see how they tackle) but they are core ones. As discussed more in Why Figma Wins, if these work they help expand the ecosystems around Figma, enabling users with new abilities and ways to engage with each other. An ecosystem also creates both defensibility and extensibility for Figma.

Beyond design and productivity, many companies today are right at the crux of these decisions. Getting a product’s core loop to work is a tremendous effort and very rare. For those who do, they are then faced with the question of what comes next.

These companies can (and have) comfortably gotten to single digit billions in valuation on their core products. If they want to go public or be acquired, they can do that. But they are also at the point where they can catch their breath, take a step back, and think about what the next decade of their trajectory looks like and what would be next in their roadmap’s sequencing if they were ambitious. For most of them, it will involve fundamental expansions of their atomic concepts. Going multi-product or becoming a platform is the key to compounding into significantly more meaningful companies.

For all the discussion on strategy, running an actual startup is often more a test of tactics and execution than strategy. One of the few exceptions to this is when companies are making new additions to their most core loops. Pre-product market fit is the most common of these moments. But the transition from a single product to a platform (or multi-product) is another common one that most successful companies experience.

Figma and Canva are examples of companies going through this expansion, but they are far from alone. Across the industry you can see a cohort of tech companies at this stage. Companies like Notion, Airtable, and Flexport are all beginning their explorations of the next major expansion of their products and platforms. While not done, they have been successful in building out their core product. As they think about their ambitions for the next decade, they will have to extend their product in fundamental ways.

Final thoughts

Often the smell test of a company is how easily it can be dimensionally reduced. It’s like some variant of Kolmogorov complexity. How few core elements can maximally explain it? People fairly push back that companies are intrinsically messy and cannot be compressed in this way. It is often true that VCs and outsiders simplify their view of companies in ways that are easier to remember but useless in practice. The flaws in this dimensionality reduction aren’t reasons to ignore it—they are the reason it is important.

As a founder, nobody is going to understand the full nuance of your company like you will. Everyone else does see a simplified, compressed, and sadly imperfect shadow of your company. Founders repeatedly underestimate the degree to which their products are complex and opaque to outsiders, because they have it fully loaded in cache. They have seen every iteration and revision and imagined in painful detail all the alternate lives their product could have lived.

Most users never talk to someone at a company. Even if they do, the vast majority of their interactions with a company are with the product. Your users know nothing about how your company operates. They don’t see all the late night whiteboarding sessions and careful deliberations that led to the specifics of each feature they use or the many iterations that were tested and rolled back and refined. They often only understand half of how your product can be used, much less your vision for how it should be used as it matures. And your future potential users don’t even know you exist.

As product becomes the driver of most interactions with a company, external gatekeepers and proselytizers like journalists and bankers become less important. Instead, it’s the clarity of a company’s product and product—and founder—driven distribution that become most key. We’re still early on in companies internalizing this.

This clarity is not just for users. It’s even more important for employees. They are the people who build complex compounds around these atomic concepts, and their misunderstandings are the root of future deviations and issues that arise. Founders get advice to repeat what matters more regularly than they think they need to. Repetition may help employees remember what’s important, but it pales in comparison to the clarity that comes from having strong atomic concepts to begin with. Like memes, simplicity is what makes them so transmissible.

One exercise I’ve often found useful for CEOs to do with their co-founders and team is to ask an important question about the company—and see how much everyone’s answers differ. People are always shocked at how much they differ from even their co-founder. It’s natural to have differences and that doesn’t even mean either person is wrong. But these unexpected differences in how to think about the company are the underlying faultlines that make it difficult to synchronize as a company on what matters and to have a common framework by which to discuss and debate important decisions.

All of this shouldn’t be misinterpreted. Very few companies come out of the womb with crisp atomic concepts. The nature of building a company is messy and complicated. Critics are right to say that many analyses over-simplify and give post hoc explanations of how to think about companies (yours truly included).

But the process of examining that complexity and finding the most lossless ways to dimensionality reduce is not the province of armchair analysts. It’s essential for founders and companies themselves to regularly do this refactoring. Just as companies build up technical debt, so too do they build up narrative debt.

Typically fundraising is a natural fitness function for doing this refactoring. For top companies this is increasingly no longer true—but the importance of this clean up has not shrunk. Whether for the sake of their users and employees—or so they can expand into becoming more complex platforms—companies must grapple with who they truly are, before they can go after who they want to be.

Appendix: Figma’s ecosystem and open source

There is a lot more that can be discussed on the platform ecosystem chart that is out of scope of this essay. This is a highly simplified chart, but it is one that comes to mind often when talking with founders of companies that are beginning to think through sequencing from single product companies to platforms. And are seeking a framework to think about their ecosystems (or analyze others) in a more structured way.

These charts can look very distinct for different companies. And even for the same company it moves over time as their user base shifts and they shape their ecosystem. Companies make intentional choices that have large impacts on what their platforms look like.

Figma is a good example of this. Unlike many platforms, Figma’s plugins and community initiatives put a large focus on being accessible to individual designers building out solutions to their own problems, whether just for themselves or to share freely with others. This focus is at odds with many other platforms that are mainly meant to be used by third party companies building products to be sold to users on top of the platform.

One impact of this is a bet on the importance of the long tail of niche use cases in Figma as seen below. There are many use cases that often are too niche to be supported as products to purchase that never are addressed in most platforms. But by making it easy for individuals or companies to build their own plugins, Figma hopes to see even these be addressed—and then shared out with the community in the way we see it often in the open source developer ecosystem.

Perfectly balanced, as all things should be

Acknowledgements

Many thanks to Keila Fong and Eugene Wei for the many discussions about this topic and help with this piece.

Additionally, thanks to Casey Winters for the many discussions about Figma and Canva. And our discussions for many years on these very topics.

Thanks also to Fareed Mosavat and Brian Balfour at Reforge. The Advanced Growth Strategy course was the origin of many conversations about Figma’s loops. And I still teach the Figma case study every semester. If interested in many of the areas in this piece, Reforge is the best place to learn them but also from people who’ve spent far more time actually putting them to practice in companies than me.

All graphics in this piece were created with Procreate and Figma. Procreate is a fantastic drawing app for iPad. If you have made it all the way through this essay and don’t know what Figma is then I don’t know what to tell you. Once again will put out into the world how much I want an integration between these two. What is the point of Figma’s platform solving for long tail niche use cases, if not to solve primarily for my long tail niche use cases.

In Formula 1 racing, you can win a world championship as a driver with one team but then not even make the top 10 without that team’s car and infrastructure. Venture can often feel like this, too. Many top performing VCs would struggle if they weren’t on their firm’s platform. And similarly, a far greater number of VCs might be able to do well if they were just at a firm with a strong enough brand. Most special are those that are the source of their own success.

In Making Uncommon Knowledge Common, I wrote about Rich Barton because he’s one of the rare founders (or investors) with the demonstrated ability to create multiple billion dollar companies. Unpacking and learning from the few who have shown repeatable and internally compounding approaches to building companies is important.

Unlike consumer, traditional enterprise markets lend themselves more naturally to deterministic and repeatable success. There’s a small handful of VCs who have clearly shown they can succeed repeatedly and whose approaches and playbooks are legible enough to imply it’s not a fluke. Speiser is one of them.

Speiser’s portfolio includes companies like Pure Storage and Snowflake Computing. It’s worth noting that Snowflake not only IPO’d and is now at a market cap of over $60B but Speiser and Sutter Hill Ventures owned more than 20% of the company leading up to the IPO. When Pure Storage went public, Sutter Hill held more than 25%. Speiser may have the highest percentage of portfolio companies that have become multi-billion dollar companies—and that trend looks to continue with his newer companies.

But impressive returns are not solely what matters for the industry. It’s tempting to evaluate firms by their returns, and from the LP perspective that may be the correct metric. But another, and more important way to judge VC firms is by the value they add above replacement to their portfolio companies. How much do they help their portfolio companies increase their likelihood and magnitude of success? Firms do this most notably by providing capital, but also by other methods like lending their brand or directly helping with operations.

For founders, this value added is what matters. The returns of a VC firm only matter to a startup insofar as they translate into improved brand, network, or access to capital for the startup. A firm’s financial performance is a reasonable signal that they may add real value and be worth partnering with, especially since some aspects like brand strength for recruiting, future financing, and customer development are a function of perceived firm success. But to prospective portfolio companies, a fund’s returns are important only as a means, not an end.

What makes Speiser intriguing is how distinct his approach is from other VCs. The tantalizing clues suggest that he has figured something out that nobody else has: the formula for creating successful companies from scratch.

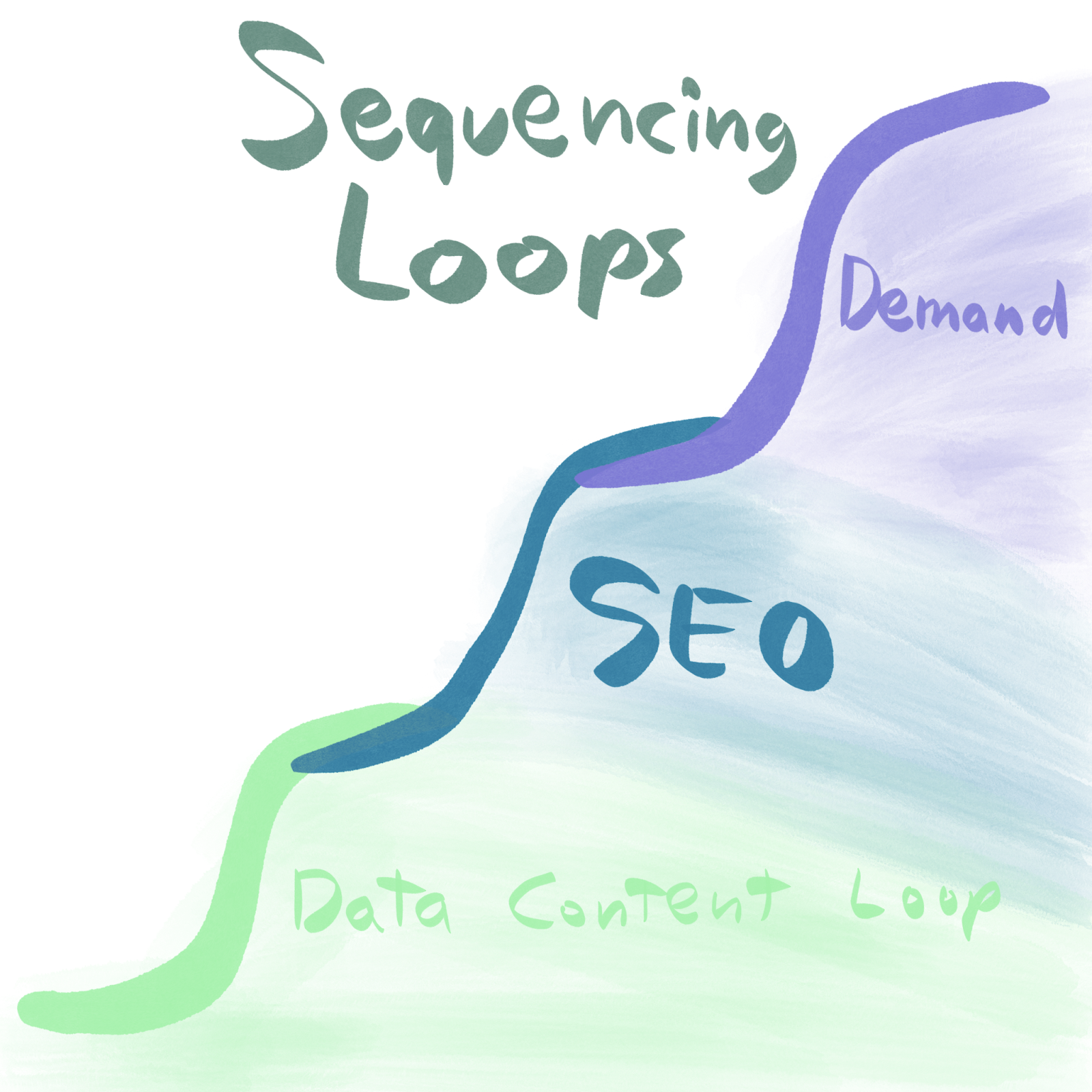

you didn’t really think there wasn’t going to be a drawing of a loop did you?

The Speiser playbook

At the core of Speiser’s approach is incubating companies, or “originating companies” in Sutter Hill nomenclature. Instead of investing in existing companies, Speiser stays solely focused on one thing: starting and building companies. Even among others who have been very successful at incubations, he is the most singularly focused on this.

bespoke artisanal charts as a service